Approximately 1 to 2 percent of the relevant deal flow for a VC firm will become a portfolio company. Hence, rejecting entrepreneurs is something a VC professional will have to do as part of his job.

This blog originally appeard on VEECEE. Also read: Understanding reasons for VC rejections – Why are you different?

As most people have an intrinsic urge to be liked, I believe most VCs want to be honest about their rejections. However, the honest opinion isn’t always appreciated. For that sake, let us clarify some reasons VCs reject your company.

One of the things a VC is really interested in is: do you fit a fund’s focus? (phase, financials, vision, personalities). For starters, it is incredibly hard to find out if your company is the perfect fit for a certain fund.

VC websites are mostly flashy, but their specific focus isn’t always crystal clear. Most funds don’t tell you what they are not interested in. Please don’t blame us VC’s for the vagueness however, as not everything in the world of startups and funding is carved in stone.

Focus fit

It seems evident that a B2C tech company will not be funded by a life science VC fund, as the focus of the fund is different.

The ‘focus fit issue’ is however much more present in the details. A tech VC with a preference for marketplace companies wouldn’t for example be the ideal fit for the B2C company. But if the dynamics of the company fit to what the VC invests in on a regular basis, there is still a chance the company would comply with the fund.

Phase fit

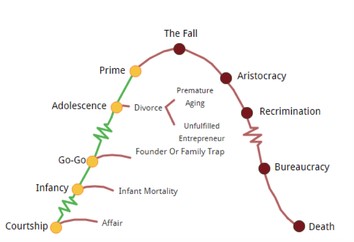

Everyone knows companies go through different phases. (I like the Adizes Corporate Life Cycle model, see picture below). VC’s usually believe they can add the most value to companies in a certain phase.

If your company is in the ‘Go-Go phase’, an early stage investor with a high risk profile probably won’t fit as a funder to your business. This particular VC wouldn’t fully understand the challenges you are facing in this phase. Vice versa, a growth investor will not have the right knowledge for ‘the infancy stage’.

The phase a company is in is however not primarily determined by revenue, this is a misconception VCs often come across. It is about proof of the product-market fit, and proof of the growth model.

{kind=link}

Finance fit

The financial needs and figures of a business must fit the VC’s and fund’s standards as regards how much investment is granted and how the money is spent. A €100M fund is for example not likely to do go for a ‘small’ half a million euro investment.

Some funds are fine with buying shares from founders, others aren’t. Some funds only go for minority stakes, some only majority stakes. Expectations regarding the financial details are best to be discussed early in a deal process to prevent surprises later on.

Vision fit

VC’s and startups should have a ‘generic vision fit’ for the goals of the business on the long term. Startups for example often want work towards an IPO. During the process of building a company, new investors may however come along as well as possible acquisition offers. In those specific cases illiquid investments may become cash, and investments become returns. Then a clear vision is needed.

Personality fit

Companies and VC funds are in essence only people. Even though doing business requires a rational approach, a business relationship often turns out to be as intense as a marriage. Having a great personality is therefore a top requirement for running a good business.

The personality fit is something VC’s put quite some thought in, but don’t really speak up about – we can’t all be BFFs can we?

Figuring out if the right fit is a matter of doing your homework: ask questions and pay attention to the details.

This guestpost is written by Mathijs de Wit, investment manager at Newion Investments. It originally appeared on the blog of VeeCee, a platform for Dutch VCs.

{kind=link}